Rasmus Corlin Christensen quoted in ICIJ article

ICTD researcher Rasmus Corlin Christensen spoke to the International Consortium of Investigative Journalists and was quoted in their article, “Crumbling Economies Must Tackle Tax Evasion To Meet Coronavirus Crisis, Experts Warn“.

Tax Notes writes article based on ICTD Working Paper

Ahead of the OECD’s Inclusive Framework plenary in Paris, we published a policy brief by Martin Hearson and a working paper by Solomon Rukundo. Tax Notes covered Solomon Rukundo’s working paper on “Addressing the Challenges of Taxation of the Digital Economy: Lessons for African Countries”, in their news story on January 29. Read the article here.

ICTD research featured in The Economist

The Economist article “African governments are trying to collect more tax” mentions our research on effective corporate tax rates in Ethiopia and our research on taxing wealthy individuals in Uganda. Read the article here. Read the brief of the Ethiopia research here and the brief on lessons from the Uganda Revenue Authority on taxing high net worth individuals here.

Taxing Africa makes Foreign Affairs’ List of Best Books in 2019

Our book, Taxing Africa, was selected as 1 of the 3 best books on Africa in 2019 by Foreign Affairs editors and book reviewers. See the full list of books here.

NTRN third annual meeting covered in Nigerian newspapers

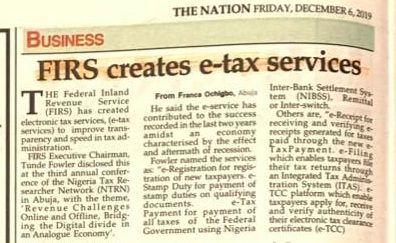

The 3rd annual meeting of the Nigerian Tax Research Network was featured in various Nigerian newspapers: The New Telegraph, The Nation, and Business Day.

Tax Matters episode on NTRN conference

This week’s Tax Matters episode covers the 3rd annual conference of the Nigerian Tax Research Network. Watch it here.

The NTRN conference in the media

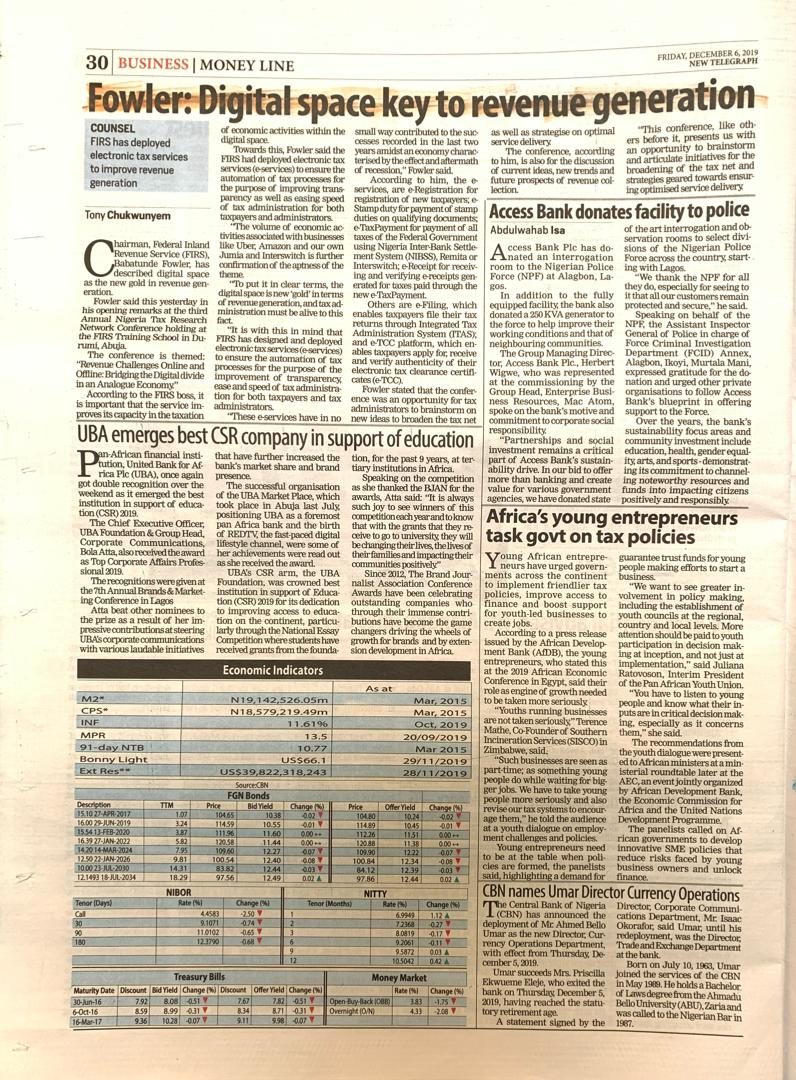

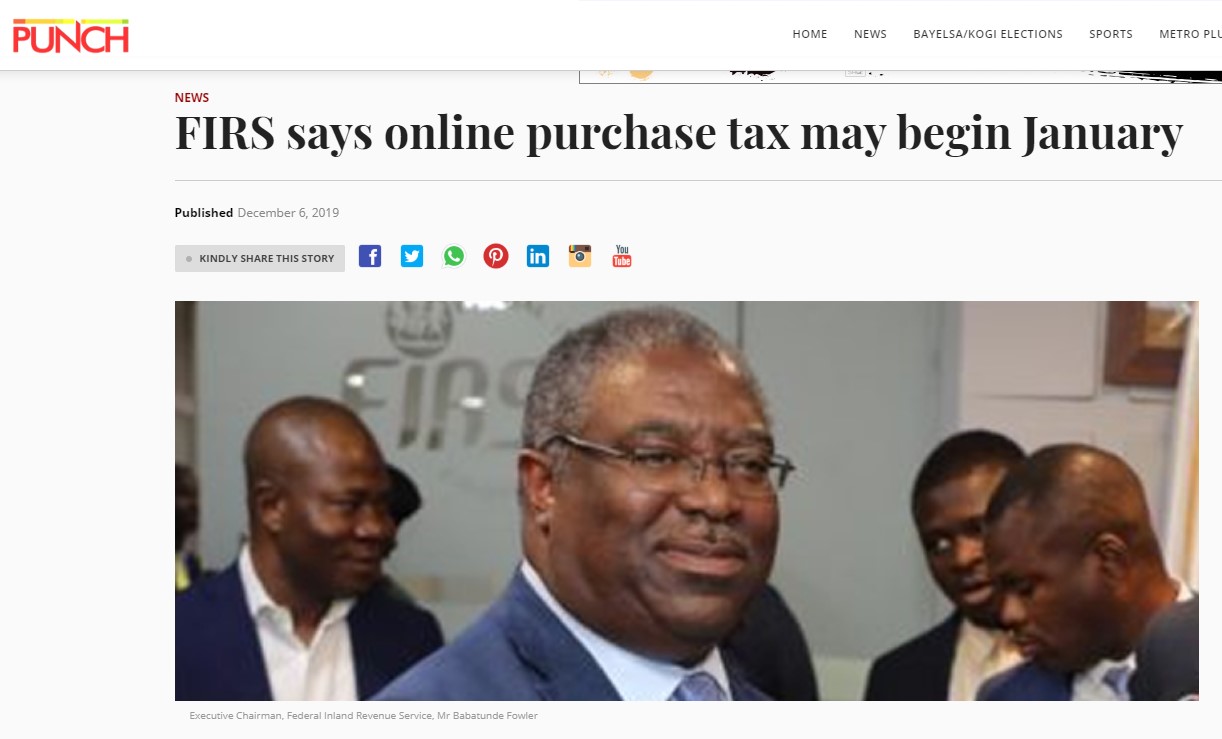

We held the third annual meeting of the Nigerian Tax Research Network in collaboration with the Federal Inland Revenue Service (FIRS) in Abuja earlier this month. Dr. Fowler, Executive Chairman of FIRS, gave the opening remarks and spoke with journalists about an online purchase tax, as a lot of products purchased online and delivered to homes across the country were not taxed. Read the articles by The Nation, Punch Nigeria, and The Daily Post.

NTRN conference featured in Leadership news

The 3rd annual meeting of the Nigerian Tax Research Network was mentioned in an article by the Leadership newspaper: “FIRS Moves To Optimise Digital Tax Collection” by Blessing Bature.

Dr. Fowler’s opening remarks at NTRN conference quoted in the news

The third annual meeting of the Nigerian Tax Research Network took place earlier this month at the FIRS Training School in Abuja. A number of researchers and policy makers gathered to discuss tax and technology in Nigeria. Dr. Babatunde Fowler, the Executive Chairman of FIRS, gave the opening remarks at the conference and was quoted in The Guardian Nigeria, All Africa, and Vanguard Nigeria.

NTRN featured on Channels Television Nigeria

The 3rd annual meeting of the Nigerian Tax Research Network was featured on Channels Television for 2:30 minutes on the 6th of December. Watch the segment below:

New ICTD research programme featured in The Exchange Africa

This month, we announced a new a 3-year research and capacity building program on tax in relation to digital financial services, and their use, as well as digital ID infrastructure, in enabling low-income countries to more efficiently and equitably raise tax revenue. Padili Mikomangwa wrote about the new research project, funded by the Bill & Melinda Gates Foundation, in their article “Africa’s digital finance research gets Bill and Melinda Gates funding“.

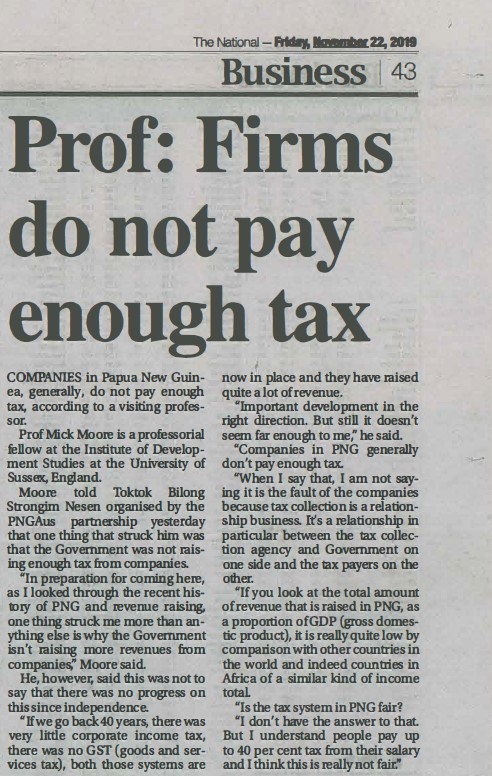

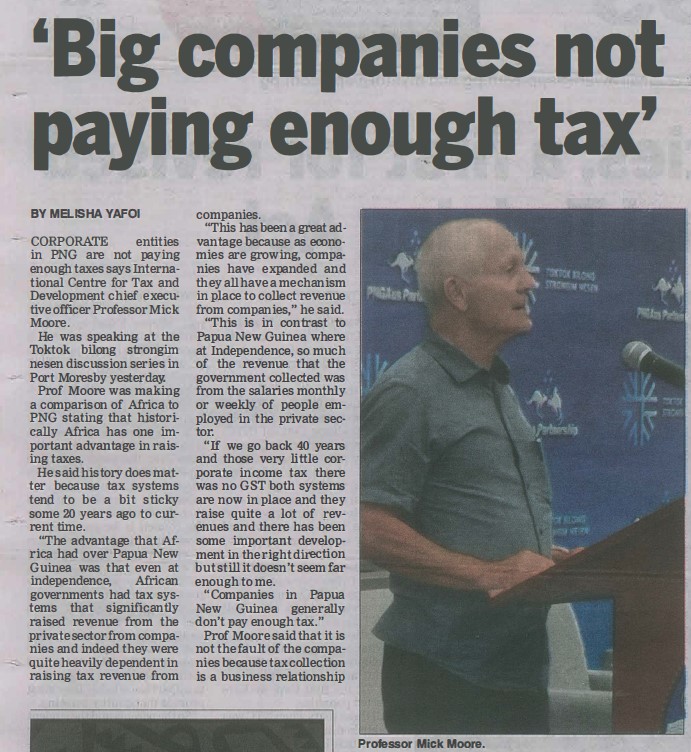

Media coverage of ICTD CEO’s visit to Papua New Guinea

ICTD CEO Mick Moore was the keynote speaker at the final session of the Toktok Bilong Strongim Nesen discussion series on “Billions from Betelnut? Taxation, Growth, and Governance“. The discussion was featured in various media outlets online and in print:

The Post Courier: Taxation is key for good governance; Big companies not paying enough tax

Loop PNG: Final Toktok Bilong Strongim Nesen series

The National: Tech, tax’s game changer