Since the turn of the millennium, the Lagos State government has made no secret of its ambitious plans to become an African ‘world class’ city, realizing its vision through borrowing as well as increased tax revenues. With 70% of the State being made up of water, land is a scarce and precious resource, so much so that it is being captured from the sea through Eko Atlantic City and other sand filling projects. Taxing land and property has therefore been central to the State government’s strategy.

The Land Use Charge (LUC) of 2001 was one of several major taxation and governance reforms associated with improved infrastructure and service provision in Lagos. That reform in itself encountered many challenges, which on the whole were effectively dealt with, leading to a rare case of relative success in property taxation in Africa – a narrative we explore in detail in this working paper. However, the recent attempt to annul the 2001 law and replace it with a new Land Use Charge law (2018) tells quite a different story.

The new law contains a number of significant and interesting changes (including some progressive measures, discussed below) but was swamped in controversy from the moment it was passed, primarily due to the combined effect of a hike in tax rates and a shift in property valuation methods. It is worth briefly examining these in turn.

The tax rate hike

The new law roughly doubled most tax rates on different forms of property, with the rate for residential owner-occupiers increasing from 0.0394% to 0.076%, for industrial properties (and residential properties occupied by owners and third parties) rising from 0.132% to 0.256%, and the rate for both commercial and ‘third party only’ residential properties rising from 0.394% to 0.76%. This continues to reflect a commitment to keeping tax rates low for owner-occupiers and charging the highest rates for revenue-generating commercial activities.

It is hardly surprising that doubling tax rates in one fell swoop was controversial, particularly in a city where land and real estate has become such a crucial (and often violently contested) source of wealth. The last time LUC rates were increased, in 2012, this was only by 5%. However, when considering why the government might have thought it feasible to make such a bold move it is worth remembering that even the post-2012 tax rates were based on a series of radical reductions negotiated in the early 2000s; in fact, the rates introduced in the 2018 law were for the most part still substantially below the ones first proposed in the 2001 law, which originally set commercial rates at 1.75% and residential (including owner-occupier) rates at 0.65%.

Opening a can of worms called ‘market value’

What is perhaps more surprising – and indeed misguided – than the tax rate increases themselves was the simultaneous shift to a new method of property valuation based on market value. The combined effect of these changes led to claims that tax bills had increased by as much as 450% (with as few as 11 days’ until the payment was due) and an explosion of anger on social media. Moving towards a system of market values for property taxation is always an immensely complex and controversial measure, with particular difficulties in contexts where property transactions are often opaque and hence the establishment of ‘market value’ is especially prone to high levels of valuer discretion, influencing and inaccuracy.

In the new law, rateable values are still derived through a formula, but this is entirely different from the 2001 formula, which was based on a stagnant list held by government of average land and building values in a given neighbourhood. The 2018 law instead enshrines valuation of land and buildings by professional estate valuers appointed by the State. This allows for a subjective process that leaves ample room for inconsistencies, with no recourse to independent valuation. Interestingly, the Lagos State valuation office pushed vigorously for the new market-based assessment, which would help to restore their relevance after the 2001 law removed their role in the collection of local tenement rates (a now defunct tax that the 2001 LUC law abolished).

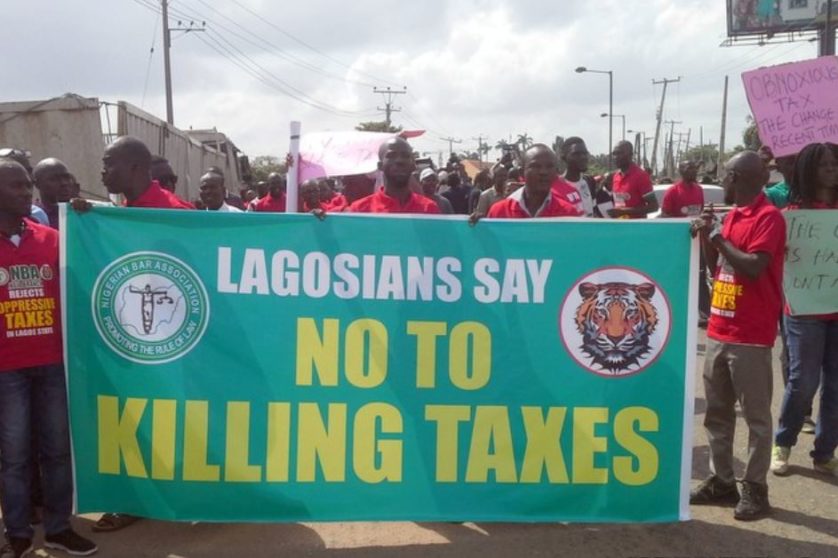

The moment the law was passed, there was intense public outcry from individuals, opposition political parties, and civic associations including the Nigerian Bar Association, Manufacturers’ Associations and the umbrella body of the Organised Private Sector. The Ikeja branch of the Nigerian Bar Association, for example, described the new law as ‘wicked, satanic and oppressive’. Adding insult to injury were highly punitive penalties for non-payment, described by the President of the Nigeria Employer Consultative Forum as ‘repugnant and odious’.

Among other things, the timing of the new law was highly questionable. The hikes came at a moment when the country was still recovering from a severe recession, and just after the Lekki Concession Company – which runs the Lekki-Epe expressway and the Lekki-Ikoyi Bridge – had increased its toll rates by up to 60%, hitting exactly the kinds of wealthy and middle class Lagosians most likely to see steep LUC increases. It was widely thought that the reason for passing the law at this time was because the leadership were trying to build up State finances in the run up to the Governorship and Presidential election to be held in 2019.

The public relations scramble

In the face of the public outcry, the State Ministry of Finance in charge of administering the LUC embarked on a series of media campaigns and stakeholder meetings to explain and justify the reforms. It was argued that the increases were necessary to fund critical infrastructure, and that the only way to generate revenue was through tax. LUC remains one of the few taxes that can be easily applied to the informal sector and unbanked citizens, making it a low hanging fruit for the State. Under mounting pressure, however, they revised the new tax rates downwards, as had happened in the early 2000s after the passing of the original 2001 law.

In the downward review there was a 50% reduction in the rate for commercial properties; 25% for properties occupied by owners and third parties (including manufacturing and industrial concerns); and 15% for owner-occupiers. This was in addition to a series of ‘relief rates’ for specific categories of people (including 10% for people over the age of 70 and people with disability) and a ‘general relief rate’ of 40% for all people paying the charge. This rendered many of the tax rates effectively quite similar to the old ones, and in the case of some kinds of property actually lower than the old ones – which was presumably a way of offsetting the much more substantial increases caused by market-based property valuations. The penalties were also waived, and the State government introduced payments by instalment.

Lagos Land Use Charge: Public Hearing Holds Amidst Protest And Chaos | Sahara Reporters https://t.co/yhAzRlleGX @followlasg @AkinwunmiAmbode @APCNigeria @OfficialPDPNig #landusecharge @lshaofficial @mudashiru_obasa pic.twitter.com/UZO78W2nuw

— Sahara Reporters (@SaharaReporters) March 27, 2018

Getting the politics wrong

It may well be that, based on their earlier experience in the early 2000s, the government always intended to backtrack on the tax rates, and were using the combination of a rate hike and the shift to a market value-based system as a way to increase their leverage: i.e. by conceding to lower tax rates, they would still manage to push through a new system of valuation that hugely increases tax revenue. If so, it seems that this was misjudged. The downward review of tax rates was referred back to the State Assembly, and subsequently went to a public hearing which resulted in a walk-out by key stakeholders including the Nigeria Bar Association, who complained that the amended law was not being made available to them for comment and input.

NBA Ikeja Chairman, Barr. Adesina Ogunlana and Comrade Abiodun Aremu, Secretary of Joint Action Front (JAF) speaks on reason for walking out of Lagos public hearing on increased Land Use Charge @followlasg #landusecharge pic.twitter.com/qYzicU5hcW

— Sahara Reporters (@SaharaReporters) March 27, 2018

According to available information at the present time, the law has been withdrawn and is unlikely to appear again this year, with its future being very unclear. The whole episode seems to provide further indication that Governor Ambode lacks the ‘magic touch’ of his predecessors Tinubu and Fashola, who designed and implemented the original LUC reforms and were considered extremely politically astute. It is highly questionable whether trying increase LUC revenues through both rate hikes and market-based valuation was the right approach to take at this time. Of greater significance, arguably, is the very low compliance rate to LUC by citizens.

What could have been done differently?

Although exact figures are difficult to ascertain, analysis shows that the State has never recorded over 50% compliance to issued bills. As such, working on the collection and enforcement side of the property tax equation may be more important and feasible currently, especially given growing evidence that African countries with relatively uninstitutionalized property markets should simplify their valuation systems rather than make them more complex. In addition, the State claims that over 650,966 properties have been enumerated for LUC. This is not even 14% of the 4.75 million properties that the government estimates to exist in Lagos. As such, instead of a new LUC law at this time, government efforts would be better spent on capturing more properties within its net while increasing compliance for enumerated properties.

In principle, the rise in rates and move to market valuation is not a bad or unjust thing. The reality is that the vast majority of Lagosians and indeed Nigerians pay few formal taxes to the State. Out of an approximate population of 21 million residents, only 4.6 million or 21% are registered with the Lagos State Internal Revenue Service (LIRS). According to the Lagos State Commissioner for Finance, 75% of properties are worth under N10 million, meaning that that most people would be paying the basic minimum charge payable, which is specified in the law as N5000 (around US $14) annually, which is hardly unaffordable to most. Despite this, the reforms would have had a much more significant effect on Lagos’ burgeoning middle classes and wealthy elites, who are often the most vocal in their discontent and whose responses to reforms need to be carefully factored into their timing and implementation. Coming at a time when businesses and individuals are grappling with decreasing purchasing power, to introduce a law that tries to do too much at once – symbolically targeting middle-class Lagosians’ wealth with a ‘double hike’ – seems ill thought-through.

According to Sven Steinmo, “Governments need money. Modern governments need lots of money. How they get this money and whom they take it from are the two most difficult political issues faced in any modern political economy.” Evidence from both our own research and other sources suggests that ordinary people generally appreciate that taxation is necessary to live in the commercial hub, and have seen improved infrastructure over the last few years, especially regarding road networks.

However, Lagos state will be better served by increasing transparency around revenue generated and associated expenditure, as well as enforcement. As the Lagos state population continues to increase, it will need to get more creative in how it increases its taxes or risk alienating an already frustrated population. It is widely known that the State’s tax revenue has been essentially spent on debt financing and recurrent expenditure, a significant amount of which goes to salaries, travels and other overheads. Lagosians need reassurance that their hard earned funds are not being used to subsidise an over bloated government.

Watch this space

In many ways, the furore over the law and its shelving for the time being has obscured some of its more interesting and potentially progressive aspects. Unlike the previous law, the 2018 one completely exempts pensioners. Moreover, it hugely increased the tax payment on vacant properties – which under the old law were only liable for the owner-occupier rate, but under the new one would be liable to pay the commercial rate, which is ten times higher. In an over-heated property market, penalising vacant property is no bad thing. Perhaps more interesting still, the new law was payable not only by property owners but by occupiers holding a lease for ten years or more, which has fascinating implications for the relationship between tax payments and people’s sense of the their property rights – something we found to be very significant in our paper on the Lagos property tax reform story. Perhaps when the law re-emerges, potentially in a different economic and political context, there will be a whole new story to tell as the implications of these less headline-grabbing aspects of reform come to the fore.